Commodity Markets Await Impact of China's Stimulus Measures

")

Will China’s latest moves to shore up the country’s ailing property sector prove effective? And if they do, how long will it take?

The answers to these questions are critical not only for China but also for global investors across multiple sectors, given their exposure to the world’s second-largest economy.

One sector particularly affected is commodities. China’s vast industrial base and large population require substantial amounts of energy, agricultural products, and metals.

For example, China is the world’s largest consumer of iron ore, the primary raw material for producing steel, which is essential for constructing buildings, bridges, tunnels, airports, and other infrastructure.

These types of projects have experienced reduced activity amid the broader economic malaise that Chinese authorities are working to address.

One visible outcome of this slowdown is the increase in iron ore stockpiles, stored at China’s ports after unloading from ships and awaiting transport to smelters across the country.

With demand down and imports up, it’s no surprise that China’s portside inventories have risen in 2024.

One major iron ore port is Caofeidian, located near Tianjin in the Bohai Sea Rim. Cargoes arrive from major suppliers, including the world’s largest iron ore exporter, Australia.

Iron ore stockpiles at Caofeidian averaged 18 million tons in September, 22.7% higher than January, according to Ursa Space data. That figure has gone up since, averaging 20.4 million tons in the four weeks through October 24.

The data comes from Ursa Space’s weekly dataset offering volumetric measurements of iron ore stockpiles at key global locations. This subscription delivers unbiased and accurate data extracted from satellite imagery, which you can learn more about by watching this video.

Stockpiles are insightful because their trends reveal underlying market conditions. Levels rise when supply is greater than demand, and fall when supply is less than demand.

The same relationship drives prices, which explains why iron ore has been under pressure this year.

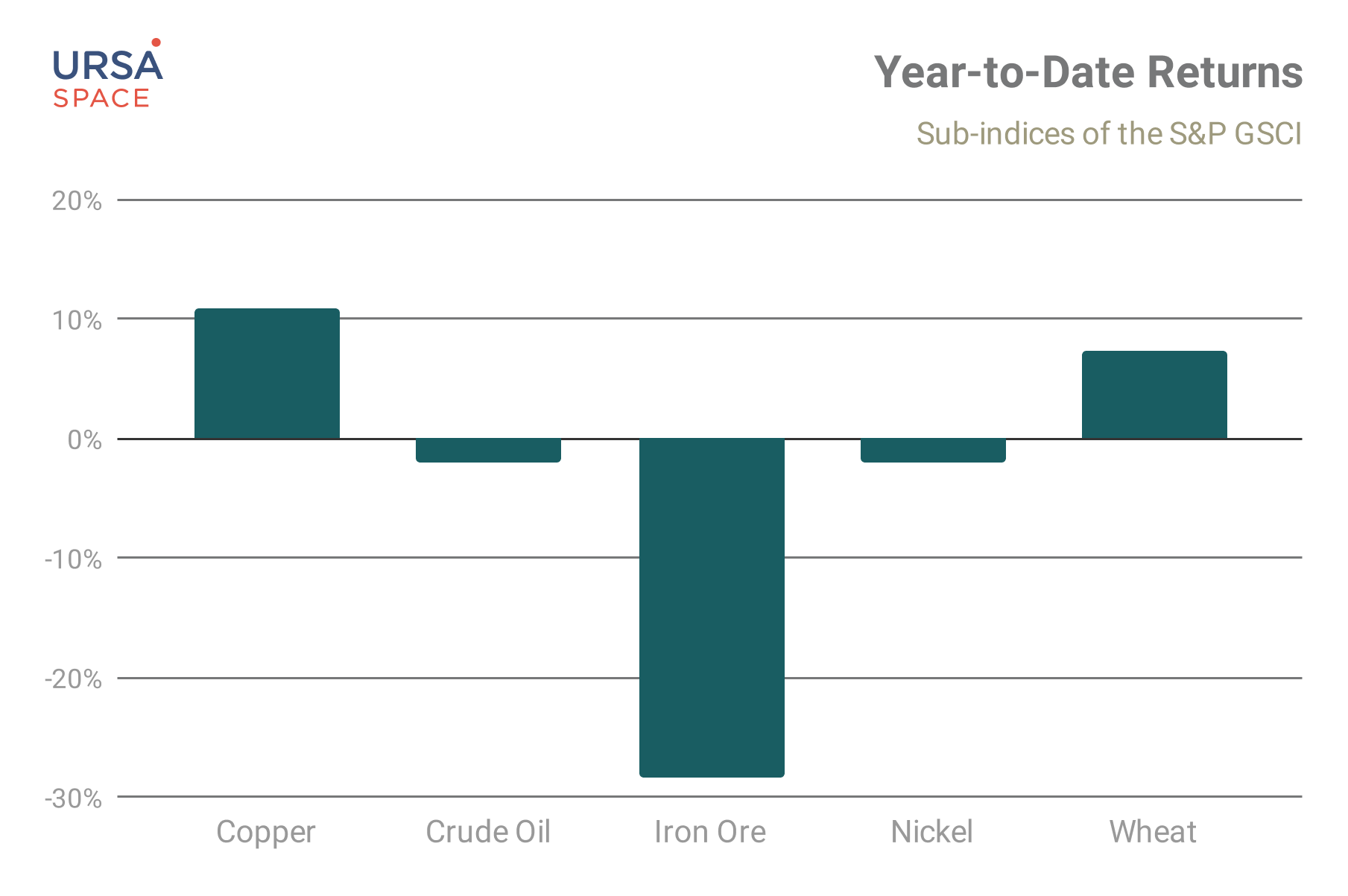

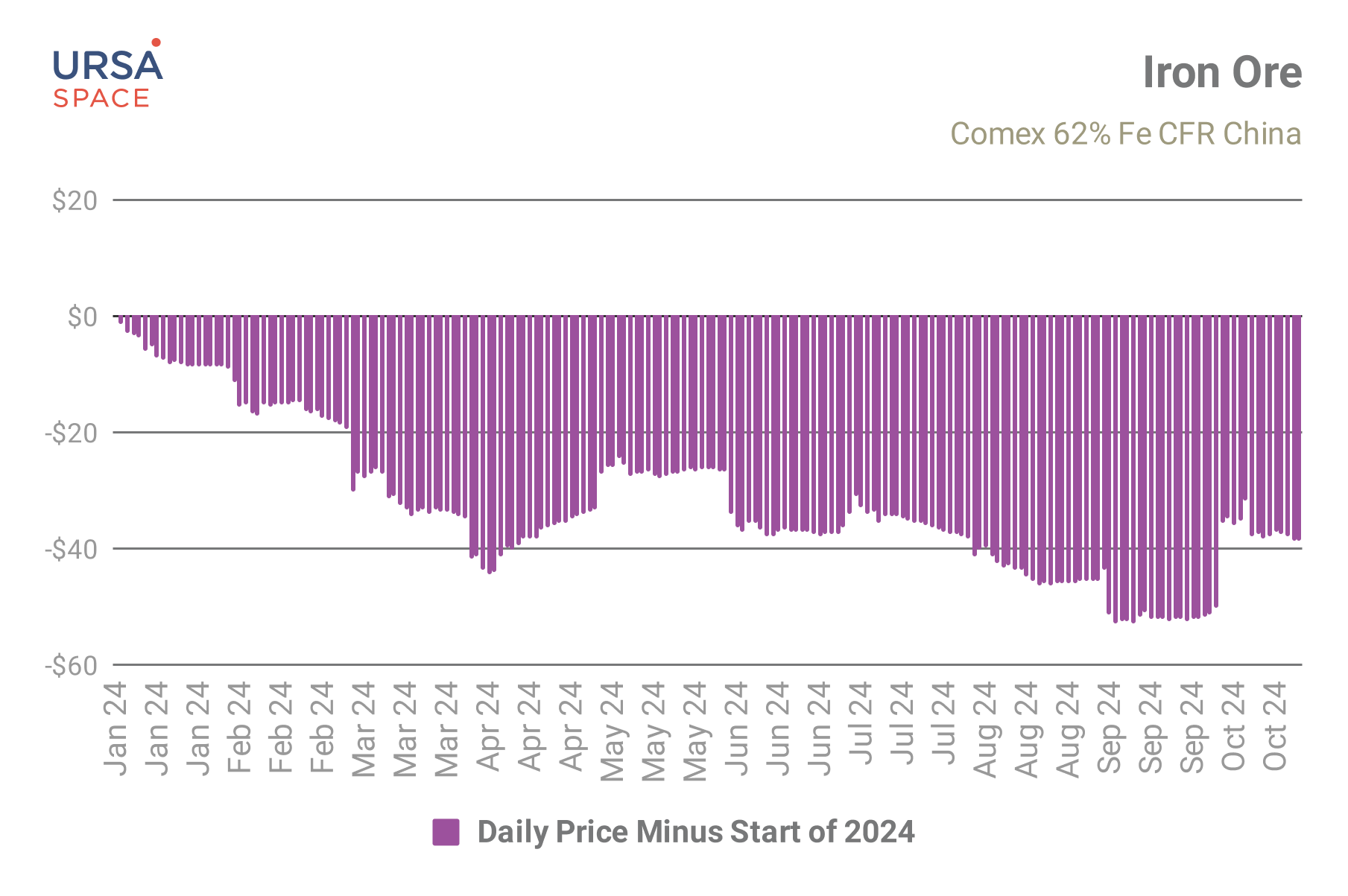

In fact, iron ore has been one of the worst-performing major commodities in 2024. As of October 24, the steelmaking ingredient was down 28.3% since the start of the year.

The losses were even steeper in September, before China announced its largest stimulus package since the COVID-19 pandemic, which briefly pushed iron ore prices back above $100 per metric ton.

However, the initial excitement quickly faded as analysts expressed skepticism, citing the need for more tangible evidence that the stimulus measures were making a difference.

“We think that the recent stimulus measures still lack detail, and we struggle to find an additional demand growth driver for industrial metals in the measures announced so far,” an ING report stated.

Iron ore futures remain nearly $40 below their value at the start of the year. Not only is weaker demand impacting prices, but so is the issue of oversupply.

Production from the "big three miners"—Vale SA, BHP Group, and Rio Tinto—has been notably strong. In Port Hedland, a major bulk export hub in Western Australia, iron ore exports to China were 12.9% higher in September compared to the same period last year.

China's total iron ore imports were 5.2% higher in the first eight months of 2024 than in the same period in 2023, despite a slowdown in steelmaking caused by weak margins.

If the stimulus measures were to work, then steelmaking profits would increase, leading to greater iron ore demand and, therefore, a decline in stockpiles.

Alternatively, iron ore stockpiles that continue to rise would suggest that stimulus measures aren’t having their intended effect.

Either way, inventories are a key indicator to watch.